Couple feel 'robbed' by 25% interest TD car loan

Dealership promised relief after a year but didn't deliver, customers say

A B.C. couple are speaking out about how they feel they were misled into a 25 per cent vehicle loan from TD, which has left them paying more than double the price of their car.

“We’re paying $21,000 for the loan — then $23,000 in interest,” said Angie Hauser of Kelowna. “They’re making money off of people who have no money.”

“We’ve been robbed by a bank with the help of a car dealer. I mean, that’s the only way I see it,” said her husband Enzo Gamarra.

"Why would I want to pay $44,000 for a car that's now only worth $15,000?"

Hauser and Gamarra are among a growing number of Canadians without adequate credit who are being signed up for subprime bank loans by car dealerships.

"I went in willingly to get the loan, because we needed a car. But, from what I was told and what I was promised when I went in — now I feel like I've been lied to," said Hauser, who insists they were assured their interest rate could be lowered, substantially, after a year.

"It's been more than 30 months. We never missed a payment, and we still have the same car and we still have the same high interest," said Gamarra.

Banks in the business

Increasingly, Canada’s major banks are behind high-interest loans such as theirs. TD has become one of the bigger players in recent years, since acquiring car financing companies in Canada and the U.S.

Dealers typically take a cut when the financing is approved, by marking up the loan amount, or from referral fees paid by the lender.

TD says its auto finance division now has $14.3 billion in "indirect" loans brokered by dealers on its books, which is up three per cent over last year.

Submit your story ideas:

Go Public is an investigative news segment on CBC-TV, radio and the web.

We tell your stories and hold the powers that be accountable.

We want to hear from people across the country with stories they want to make public.

Submit your story ideas to Kathy Tomlinson at Go Public

Follow @CBCGoPublic on Twitter

That money was loaned to both regular and subprime borrowers, the latter being people who don’t have adequate credit ratings to qualify for regular financing.

"Subprime" became a household term after the economic crisis of 2008, which was partly caused by defaults on high-risk mortgages in the U.S.

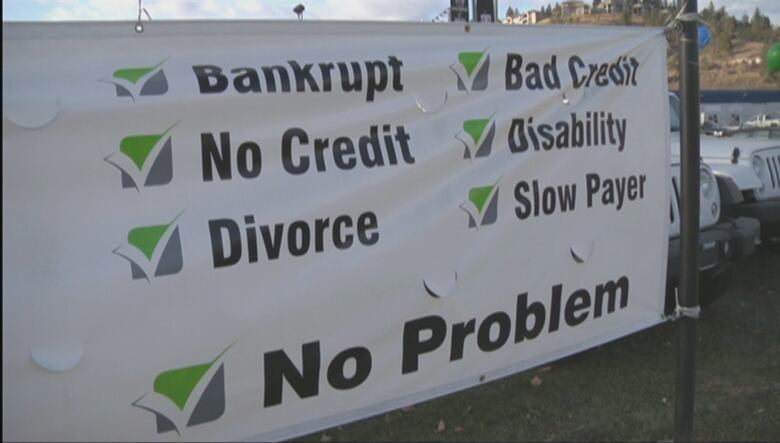

Hauser and Gamarra declared bankruptcy in 2010 over credit card debt. The following year, they saw a sign at a Kelowna dealership offering financing for people with bad credit.

“We wanted to get a reliable car for our family,” said Hauser.

No other financing available

She manages a beauty supply company and her husband is a courier. They have a four-year-old daughter.

At the time they got the loan, they said, their car had broken down beyond repair.

They said they had no money saved for another car, but they needed one to get to work, so financing was their only option.

“I know it’s our fault we got into it, but it’s ridiculous. It’s like rich people getting rich off the poor,” said Hauser. “It’s a way to loan-shark, legally.”

They said Okanagan Chrysler Jeep Dodge sold them a 2010 Dodge Avenger, by promising them if they made their payments faithfully for a year, the dealer would then secure another TD loan, perhaps on a trade-in, at a much lower interest rate.

“We had to get the car they wanted … we didn’t even get to choose the car that we purchased,” said Hauser, despite their preference for a lower-priced model.

“We worked so hard to make these perfect payments so we could get refinanced.”

After a year, records show the couple went back to the dealership and directly to TD, asking for better terms.

They said they were shocked when they were told they still couldn’t get an affordable rate, because of their bankruptcy.

“How can you deny me refinancing when I’ve been in bankruptcy when you gave me a loan in bankruptcy? It doesn’t make sense,” said Hauser.

TD loans officer surprised

At first, Hauser said, the loan officer they met with at the local TD Canada Trust branch didn’t even believe the bank could charge 25 per cent interest.

“And then he went through the paperwork we had, and said 'I can’t believe TD did a loan like this,'” she said.

TD Auto Finance then sent a letter denying their request for refinancing.

The couple also went to another dealership, asking for a trade-in and new financing. They said that dealer arranged another loan, also from TD, at 15 per cent interest, including the dealership's cut.

The loan term was shorter, however, with higher monthly payments, so they couldn't afford that either. That left them locked into the full term of the original 25 per cent loan — a total of seven years.

“It’s grocery money, it’s money for my daughter. It’s just so stressful I can’t even explain what it does to us,” said Hauser, in tears.

She said the payments eat up one-quarter of her take-home pay.

“We are talking about a big Canadian bank. And I mean for them to do that to us … that just makes me angry,” said Gamarra.

Questions unanswered

TD refused to discuss this case, citing privacy, even though the couple were willing to give their permission.

It also refused to answer Go Public's questions when we asked how many subprime auto loans it has issued in recent years, how much money it makes from them — and how it justifies charging 25 per cent interest, particularly when there is a vehicle for collateral.

“TD Auto Finance offers a full spectrum of auto lending options, including non-prime loans in some markets,” said a statement from the bank.

“In Canada, we have a mature non-prime business … we have rigorous lending criteria and we only lend to those who fit within our risk appetite and satisfy thorough qualification criteria.”

According to Canadian Auto World magazine, subprime loans make up approximately 25 per cent of all auto loans arranged by dealerships.

If 25 per cent of TD’s $14 billion in indirect auto loans are subprime, with roughly the same terms Hauser and Gamarra have, the bank would stand to make approximately half a billion dollars a year, in interest payments alone — if all of the customers made their payments.

“I mean, not even credit cards charge that much,” said Gamarra, who said the fact they've made all their payments should count for more.

Risk low to banks

According to the Canadian Auto Dealers Association, delinquencies on all auto loans are at an all-time low.

The industry attributes that partly to relatively low monthly payments, stretched over terms as long as eight years. That also means many people owe — and pay — much more than their cars are worth.

The Canadian Banker's Association refused to answer questions about rates, but sent a statement also stressing that default levels are low.

"Banks in Canada are prudent lenders, and manage risk carefully and make sure borrowers are properly qualified and can withstand economic fluctuations," said CBA spokeswoman Kate Payne.

"Banks only lend to those who they believe can pay the money back, and the numbers back this up."

“A 25 per cent interest rate is predatory,” said Hugh MacKenzie, a Toronto-based economist and public policy consultant.

“That’s a ridiculous interest rate to be paying, particularly for a car, because a car can be repossessed if you don’t make the payments.”

He said low default rates are another reason why the high interest isn’t justified.

MacKenzie is the former chair of the Atkinson Foundation, which promotes social justice. It recently funded research — and education for shareholders — about the Canadian banks’ involvement in the subprime lending industry.

An "issue brief" from that research said, “There are significant risks, particularly for banks, of being associated with subprime lending activities leading to negative public perceptions and increased distrust of these financial institutions.”

MacKenzie said Ottawa should step in to regulate the interest rates, especially given the finance minister's expressed concern about record consumer debt levels.

“[The couple] would have gotten a cheaper loan if they had used Visa to buy the car. And yet people are complaining — and the federal government is expressing concern — about high credit card interest rates.”

Ottawa will 'monitor'

The federal Finance Department sent a statement indicating the government is not considering any action.

“The government will continue to carefully monitor the types of financial products and services available to Canadians in the marketplace, including those related to vehicle financing,” said the statement.

In the meantime, auto sales in every Canadian province increased from 2012 to 2013. The industry is attributing some of that to subprime lending.

Since Go Public got involved in the Kelowna couple’s case, Hauser said the dealership has called several times and has offered them a new loan — for a new car — at 4.99 per cent interest.

Okanagan Chrysler’s general manager declined an interview, but in a statement he said he will do what he can.

“We are willing to work with this customer and the lender to see if their rate can be improved, and shall do so, but as we do not control the rates we can only do our best,” said Clayton Andres.

Hauser, meanwhile, thinks the subprime market needs closer regulation.

“I think that the government should regulate these loans or regulate these banks and watch what they are doing a little closely. Because the banks don’t even know what’s going on with their own loans,” said Hauser.

Submit your story ideas to Kathy Tomlinson at Go Public

Follow @CBCGoPublic on Twitter

ABOUT THE AUTHOR