Be very afraid of the Canadian housing bubble

I want you to be afraid. Very afraid of the Canadian housing market.

I want people who are considering buying a house in Canada to be the most frightened. People who just bought a house also have every right to be nervous. But even if you don't have a stake in the property market, I would like you, too, to be fearful of a bubble in Canadian property.

I'm frightened myself. A lot of smart people are. But I should make it very clear I've no desire to be the Nouriel Roubini of the Canadian housing market.

Roubini, for those who didn't notice, rose from B-team academic to A-list fame and fortune by predicting the U.S. housing and market collapse of 2008.

Before the crash, he was just one more Chicken Little – that children's story character, who, after being whacked by a falling acorn runs about shrieking, "The sky is falling, we must run and tell the King."

After the crash, Chicken Little no more, Roubini was Solomon the Wise. Having demonstrated his credentials, Roubini is still travelling the world, dining out as The Man Who Got It Right.

When doomsters are right, they are showered with honours. Think of how religious enthusiast Harold Camping's star would have risen had the world actually ended last May.

But I don't want that for me. I just want you to be frightened.

Time to panic?

Right now in Canada we are at the Chicken Little stage. The real estate industry and the banks say there is no bubble. Our finance minister, Jim Flaherty, has warned repeatedly about high debt levels, but even he is on the record saying there's no bubble.

I don't want you to listen to them. I want you to listen to the Economist, Canadian Business, the Wall Street Journal — each of which have sounded scary warnings. Macleans magazine went a step farther with a screaming headline saying it was "Time to Panic."

When I saw that one, I pictured readers taking the advice – wide-eyed, shrieking, hyperventilating, running aimlessly back and forth – and wondered at the advantages of being advised to panic, no matter what horror might be in store. But I liked the tone. It was frightening.

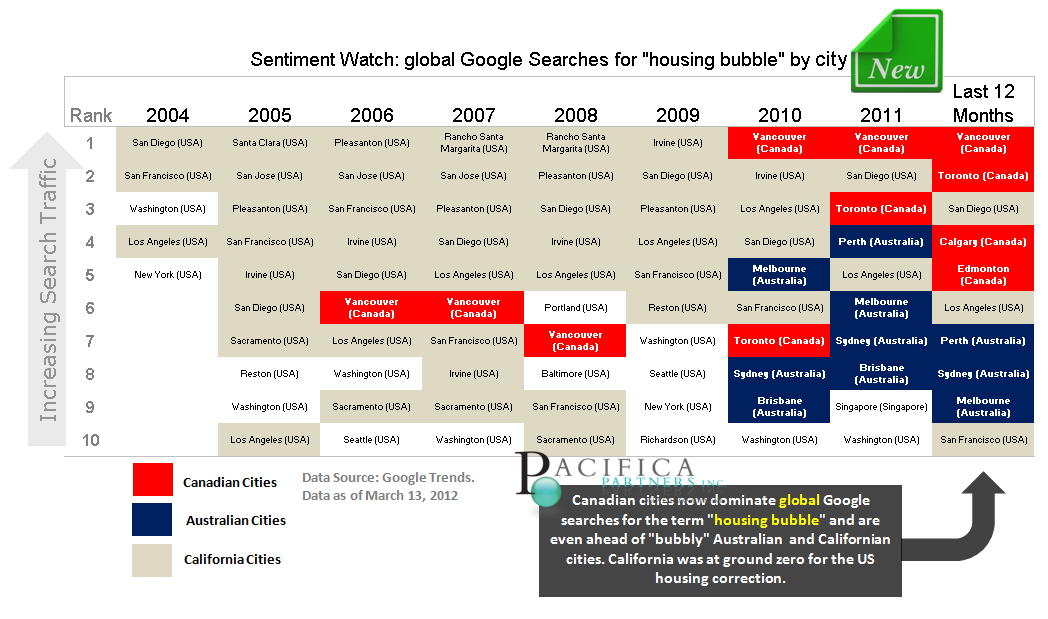

The investment site Seeking Alpha had a wonderfully terrifying chart. Using the same kind of analysis that warns of flu outbreaks before health officers know they are coming, the chart analyzed Google data to show a rising number of searches in Vancouver, Toronto, Calgary and Edmonton for the term "housing bubble."

{kind=link}

The chart shows that a similar searching pattern happened in 2007 at the epicentre of the U.S. property earthquake.

Now here is my dirty little secret: I am not convinced we are in the midst of a property bubble.

I have lived in Hong Kong. I have lived in southern England. I have seen property prices go very, very high and, apart from little downward blips, stay high for years. I know that middle-class Canadian homeowners will do almost anything to avoid defaulting on their mortgages.

Canadians different from Americans

Unlike in the United States, it is very hard for Canadians to walk away from their mortgage responsibilities. Mortgage insurance protects your bank, not you. Here, a default is not a get out of jail free card.

In Canada, mortgage interest cannot be deducted from your taxes. Instead, we only benefit by getting tax-free capital gains after you sell.

I know that the Canadian mortgage market is not the wild west that it was in the United States in 2007. I know that the U.S. central bank, which effectively controls our mortgage rates, is planning to keep money cheap until at least 2014.

I know that markets can go up, and up, for a long time without crashing. I know that the only proof of a bubble is when it pops.

But at the same time, when I look at my own neighbourhood, my fear grows. Houses listed for sale are gone within a week. "Sold over asking price" shingles dangle from the real estate signs. Condos climb out of the ground everywhere and the builders say they have buyers.

It seems clear to me that people haven't been listening to the dire warnings.

And that is why I want to spread fear. Because though we may not be in a bubble now, if we keep this up, we are going to be. And if a bubble pops, that is something really worth being frightened of.

Look at this sentence from last Thursday's main editorial in the Financial Times: "When house prices rise because households gorge themselves with debt, IMF researchers found, the ensuing recession is much deeper and more protracted than busts not preceded by such debt accumulation."

The logic is not too hard to see.

First-time buyers in jeopardy

When a housing bubble pops, first-time buyers with large mortgages are really screwed. Leverage is great when assets are rising, but a decline of even five percent can quickly wipe out a young family's nest egg. A drop of 10 or 20 per cent leaves many homeowners tens of thousands in the hole. Even homeowners without mortgages feel poorer – the so-called inverse wealth effect.

According to the IMF, when that happens, spending dries up for five years, and stays flat for years after. In Canada, a popped bubble will really hurt us all.

If you've suffered from government cuts, you ain't seen nothing yet. If you're unemployed, it will only get worse. If you're poor, expect to get poorer.

I hope you are truly frightened now. But no matter how frightened you are, it may be there are too many forces pushing us in the opposite direction.

Despite deep fears of their own, banks are still crazy to lend. Just as Hertz makes its money by renting cars, banks make money by renting money. They just can't help themselves. They have shown it again and again.

Low interest rates held down artificially by central banks in an attempt to jump-start the economy make the math for borrowing to buy look good, for now at least.

Longstanding folk wisdom learned from your parents and grandparents like "Why pay rent to somebody else?" or "They ain't makin' any more land" or "Safe as houses" is deeply embedded in the popular psyche and hard to shake with rational arguments.

And perhaps the worst thing: No matter how many times central bank governor Mark Carney or people like me cry wolf, the housing market disproves us, year after year, rising far above the return on other investments. But I fear that eventually, just like in the story, the wolf will come.

I don't want to become famous for predicting a bubble in the Canadian housing market. I will forego the honours. Because of my fear, I don't want it to happen at all.

But maybe fear is not enough.

ABOUT THE AUTHOR